Hi everyone—I’m so glad to have you here. What a week.

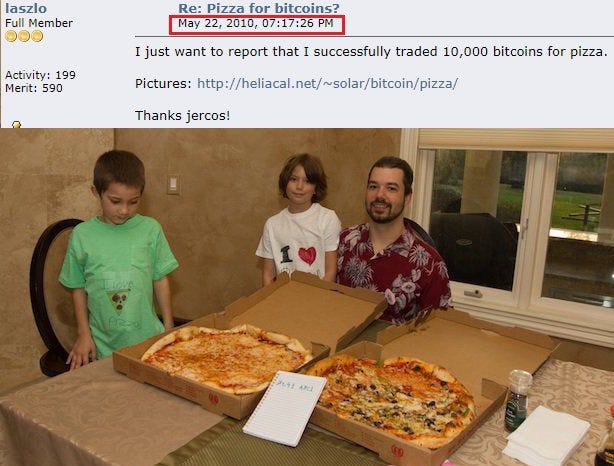

Today (May 22) is an auspicious day in bitcoin history. On this day in 2010, someone who goes by the name Laszlo spent 10,000 bitcoin to purchase 2 pizzas, marking the first recorded use of the cryptocurrency as a medium of exchange and thus giving the token a value determined by free market participants.

Right now 10,000 bitcoin has a market value of about 300 million dollars, so this pizza purchase is a fun paradoxical example of both the ability to spend bitcoin and the power of NOT spending bitcoin.

When you hold a scarce, hard-to-produce, desirable asset its value grows over long stretches of time, but the life of a human person involves expenditures such as food, clothing, and shelter. So scarce, hard, desirable assets must be parted with regularly in order to survive, grow, and flourish.

Money is not meant to be held, it’s meant to flow from person to person. But something is only considered “worth it” if the marginal value of the trade is, at that moment in time, more beneficial than simply preserving the ability to trade at a later date in the future. This is commerce. This is exchange. This is life.

Markets and exchanges are how societies became incentivized to trade with their neighbors rather than destroy them outright, since others have abilities and resources that are far easier to purchase than learn or own.

Trade, loans, investments… these are tools we use as a civilization to collectively survive. Being “civilized” means being polite and respectful, because we learned (and continue to learn, imperfectly) that cooperation leads to better survival outcomes than tit-for-tat destruction, on average.

Markets work over the long term, but over short intervals they appear chaotic, volatile, and downright problematic. Let’s have a look at today’s markets as an illustration, shall we?

The Dow Jones Industrial Average has been down 8 weeks in a row, something that has literally never happened before. And right now high yield credit default swaps are soaring past 2018 highs, which is a sign that global debt markets (which underpin global stock markets) are starting to send tremors through the system, felt most dramatically at the surface.

So when these ripples propagate into tsunami ripples at the surface—with corporate equity markets, i.e. the stock market—things get dramatic indeed:

Unfortunately, “free and open markets” are a thing of the past. A figment. A nice ideal to shoot for but something obliterated by humanity’s urge to fiddle and control. Markets today aren’t like buying a pizza with bitcoin but more like asking permission to buy a piece of pepperoni with a Dave & Buster’s token you borrowed from the janitor on interest.

This is why the Federal Reserve—a cartel of unelected bankers—uses words like “pain” to describe the impact it will have on the price of goods & services after it decides, in its infinite wisdom, to raise interest rates one quarter of one percent because they decide it’s ultimately good for the patient’s health.

The primary concern of both the Fed and the Treasury—especially with midterm elections later this year—is not to “spook” markets. To keep everyone calm and happy. They want to avoid a panic, so they can’t yell “shark!” in the water even if there is literally a shark in the water. That would terrify everyone and get them out of the water en masse, which would be great for everyone’s survival but not for the administration’s survival once election season arrives.

So instead of doing the right thing they do the right thing for them: they print.

The Senate speedily passed a $40,000,000,000 Ukraine aid bill, an example of why war (or any sufficiently large, nebulous existential threat like “disease” or “the end of the world”) is essential to justify spending with impunity and without question in order to preserve the appearance of control and stability.

They get to print money and spend it immediately, while everyone else (you & me, et al.) has to earn money and deal with the downstream inflationary impact of an inflated currency supply.

We pay taxes on our income, and also pay sales tax on what we buy with what’s left over after we pay taxes on our income, and also pay capital gains taxes on what grows in value with what we’ve purchased with our after tax income.

And all that tax revenue they’re collecting from us is still not enough. They need to also (apparently) print new money on top of that, which makes any money you and I still have left over able to buy less and less, since there are more units in the system chasing the same (or diminishing) number of goods and services.

And still they continue to raise our taxes (on account of inflation, obviously), and yet all of our roads and bridges are literally getting worse.

We may not all agree on the solution, but I think we can all agree something is very wrong.

New Zealand announced it will spend NZ$1,000,000,000 “to ease impact of faster inflation,” which is a hilariously backward strategy that I suspect the NZ government knows full well is perfectly wrong but are way past the point of even caring to pretend to tell the truth. This is how out of whack things have gotten among governments & banks looking to preserve their reign.

Then again, maybe these central bankers are indeed as out of touch with reality as they appear, and completely unaware of how the world actually works outside of their textbooks and mathematical modeling software. One screenshot making its rounds is this glimpse at Federal Reserve bankers and the jobs they have held outside of the Federal Reserve. Not encouraging. 🤔

“If there is an abundance of money, there is scarcity everywhere else.

If there is scarcity of money, there is abundance everywhere else.”

—Jeff Booth

It's been fifteen years since you could beat inflation with a savings account. The Fed has to care about the stock market (which was not and is not in the scope of its mandate) because it has, over the course of its garbage existence, forced people to buy stocks and become amateur investors just to preserve some semblance of purchasing power as the money we use to purchase things is methodically eroded.

Worse yet, the prevailing narrative that administrations in power try to push is that corporations—the actual companies in our stock portfolios—are responsible for the inflation. Corporate Greed™️, they say.

Corporations have been around for a very long time, but they only just became extremely greedy and all at the same time? Okay.

They say we’re on the verge or not on the verge of a recession, but I am here to tell you that we are absolutely in a recession despite whatever math equation they’ve devised to determine the threshold at which a “recession” is technically the term. The question is whether or not we tip into full depression later this year.

Numbers like CPI—"inflation rate”—are trailing indicators, and don’t forget that inflation compounds. To say an officially understated number like 8.3% is an inflation number that has “peaked” is misleading. (By the way, the Fed’s mandate is to keep it at 2%) The number may or may not have peaked. But enjoy the 8.3% compounding of reduction in purchasing power year after year as you try to figure it out.

Don’t wait for the news to confirm what you already suspect to be true. Numbers describing large dynamic, complex systems such as the weather or entire economies are trailing indicators to reality.

Speaking of the news: did you know that 32 central banks and 12 financial authorities—representing 44 countries in all—met in El Salvador to discuss financial inclusion, the digital economy, banking the unbanked, and the benefits of the El Salvador Bitcoin rollout?

You might be wondering why the Mainstream Corporate Ad Sales Industry didn’t cover this story on their nightly news programs, and the answer is likely to be found where most answers are found which is by asking the question: cui bono? Who benefits?

News Entertainment is owned by wealthy industrialists in positions of influence and power who sit very close to the money printer, and so have every financial incentive not to draw attention to the fact that rising nations are opting out of dollar hegemony. Dollar hegemony is what pays the bills, and nightly news depicting the escape hatch is not good for business.

In terms of actionable advice, I think C.J. Wilson has my favorite take so far, which essentially boils down to: stop being cute. Don’t invest what either you actually need or aren’t willing to lose. Hold and defend what you value. (“Hold bitcoin for liquidity.”) Borrow cheaply if you must, but focus on paying off your expensive debts. Food, clothes, shelter… don’t lose sight of what actually matters.

The Fed and the US government are not going to yell “shark!” in the water, and will certainly not encourage you to own a secure, digital, peer-to-peer money specifically designed to separate money from state.

Always ask yourself: cui bono—who benefits? It’s not in the mayor’s best interest to yell “shark!” at the beach on the Fourth of July. But that won’t stop the blood from flowing.

Until next time 🤙,

Recommended Resources For Plan ₿

Swan. I became an official Swan partner because I love them so much. So if you're like me and just want an easy, automated way to buy bitcoin on the regular with the lowest fees in the game, head to https://swanbitcoin.com/Mulvey to get $10 in bitcoin for free ✨

Fold Card. Earn bitcoin on everything. You can win up to 100% back on every purchase, and every swipe is a chance to win a whole bitcoin. I use my own Fold card to pay for almost literally everything. If you use this referral link you get 5,000 sats free ✨