“Literature is meant to be provocative, to raise doubts and to address issues that are not evident.”

—Olga Tokarczuk

Hi everyone—I’m so glad to have you here. What a week.

This week was packed with stories:

The Dow swung wildly in both directions as market gyrations saw several percentage point moves in one day. In the end, stocks experienced the worst January since 2008

Fed Chair Jerome Powell said almost literally nothing for an hour during prepared FOMC remarks as well as the live Q&A session on Wednesday

The Fed’s Neel Kashkari walked back prior comments about March rate hikes, opening the door to do or not do something in the future depending on what happens idk (You may remember Kashkari from this dystopian gem back in 2020)

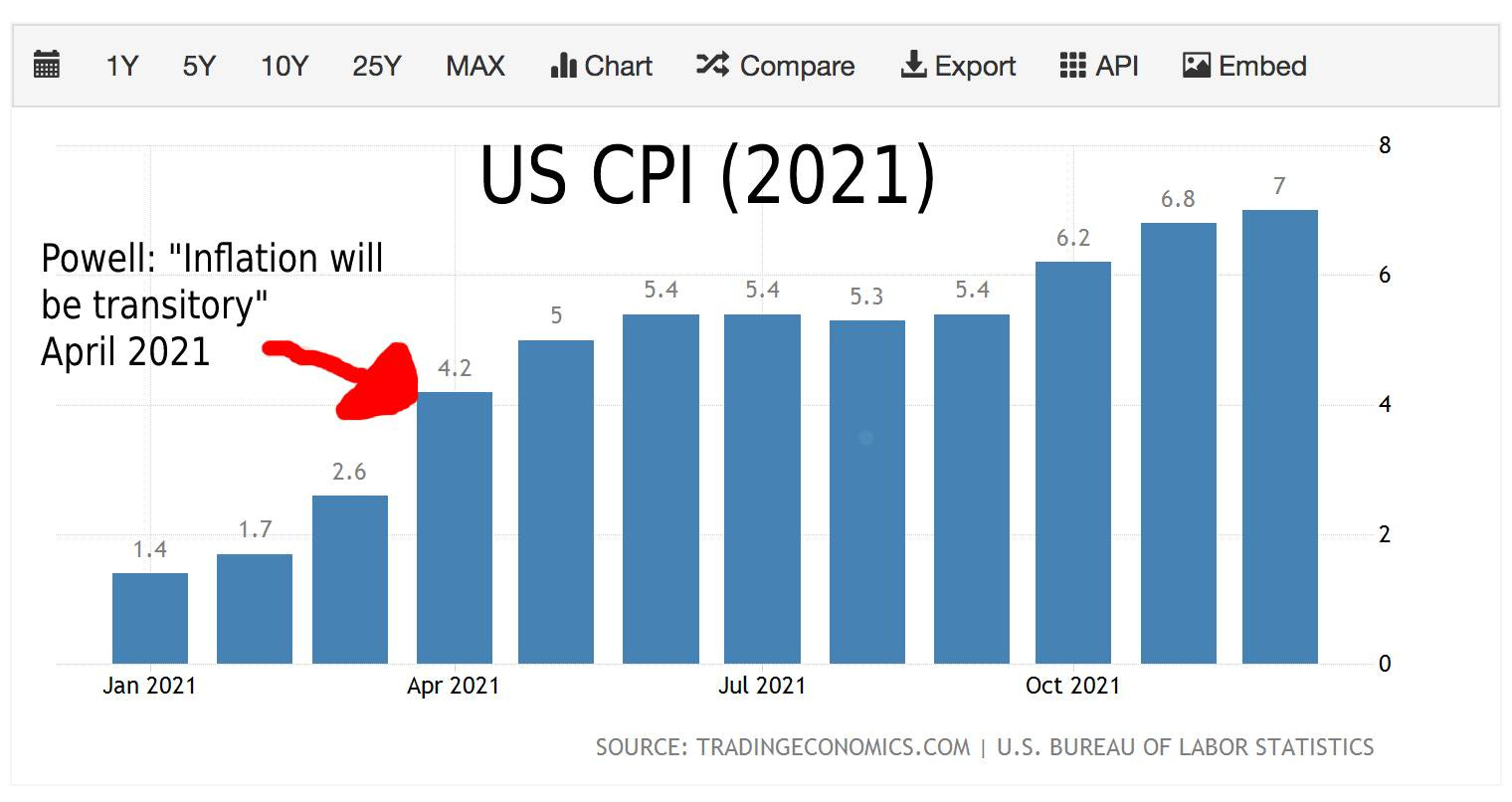

The Turkish President fired the head of his national statistics agency after publication of annual figures in early January that put Turkey annual inflation rate at 36.1%, its highest level in 19 years. We can’t have that now can we.

And get this: for the first time in the history of the 60/40 portfolio, the NASDAQ has been down more than 6% in a month while bonds have also been down. Bonds have traditionally been used as the “safe” cushion to hedge stock plunges like this. Something is deeply wrong. (One theory: “The lack of bidding you’re seeing in the bond market is because people don’t trust the currency.”)

Meanwhile, in the world of the censorship-resistant, decentralized, peer-to-peer global monetary network with a fixed supply and rules kept out of the irresponsible paws of money manipulators:

Bitcoin surpassed American Express in annual transaction volume, and more transaction volume in the fourth quarter than all credit card networks combined for the entire year when including change and intra-entity transactions

Senator Wendy Rogers introduced a bill to make Bitcoin legal tender in the state of Arizona.

It all reminds me of another story: Catch-22.

The main thrust of the plot of this classic novel, and how “catch-22” became a colloquial expression for a paradoxical pickle to find oneself in (damned if you do, damned if you don’t) is this: the main character fears his commanders more than the enemy because the commanders increase the number of required combat missions before a soldier may return home, and retroactively raise that number as soon as it’s reached.

The more missions he flies, the more missions he has to fly.

This futile loop of manipulated metrics and ever-increasing difficulty just to stay alive sounds an awful lot like our runaway inflation problem, doesn’t it?

"The Fed realizes they're in a catch-22: inflation is running rampant at the same time financial assets are at all-time highs, and they need to do something to try to bring down inflation. But as soon as they do start to tighten (which they probably will), they're gonna wind back up in the exact same place they were in September 2019 where they literally break the system.

I don't think they have that appreciation. They look around and see that the market is flooded with liquidity, but even if today—if there's $85 to $88 trillion in dollar-denominated debt—the base money is 8.4 trillion. Each dollar is lent out 10:1.

In their world they want to be reactive, they will want to do more of it and they will try, but there are certain mechanisms that will prevent that from being sustained in any meaningful way."

The thing to remember about the cartel of unelected bankers known as the Federal Reserve—which is neither a Federal institution nor holds any reserves—is that the political pressures they would face from raising interest rates are much, much larger than a tiny percentage increase in CPI inflation. “It's far easier to lie with CPI than to destroy the financial system by raising rates and putting a lot of banks out of business." As investor and macro analyst Lyn Alden put it: when push comes to shove, whenever the choice has been between crashing the market or printing more money, they print.

They are businesspeople conducting business, and we’re caught in the middle.

Thomas Mann—Nobel prize-winning author of the novels Death in Venice, Magic Mountain, Doctor Faustus, and more—had much to say about the topic of inflation, being himself a German who saw firsthand the impact of hyperinflation in the Weimar Republic following the aftermath of WWI in 1923. He explored this topic in his 1925 novella Disorder and Early Sorrow.

In this piece from The Review of Austrian Economics (which I plan to delve into in more depth on here in the future), Paul Cantor argues that Mann hit on an important insight on the relationship between truthful fictions and false realities—that inflation is a kind of reality-distortion mechanism that alters and subverts people’s ability to know what’s going on at all.

“Inflation eats away at more than people's pocketbooks; it fundamentally changes the way they view the world, ultimately weakening even their sense of reality.”

“Mann invites us to consider what happens to our lives when we are forced to take our money purely on faith and that faith is betrayed by the government.”

Notice that he’s not talking about lies per se, but rather the increasing unreliability and falseness of indictors that were previously used to judge reality, and the distrust that accumulates in a society or a system when people can’t believe anything they see, hear, or are told anymore.

Things like: markets at all-time highs and charts showing The Best Economic Performance Since 1984™ while home prices remain out of reach, used car prices are skyrocketing, supply chains remain backed up, and the country is saddled with historically high levels of debt. This is what best economic performance in decades looks like?

Nineteen Eighty-Four is right: “the novel examines the role of truth and facts within politics and the ways in which they are manipulated.”

“Markets, despite the recent correction, remain historically, horrifically overvalued”

Not to beat a dead horse or state the painfully obvious, but the stock market being at historic highs while investors are holding historic amounts of debt is, historically, not a great place to be.

To be super clear, and to return to the reason why the traditional 60/40 portfolio of stocks/bonds is completely broken:

The last time CPI was at 7%, the U.S. 10-year Treasury (the “risk-free rate of return") was yielding 9%, so a fixed income investor (i.e. bond investor) could easily earn a nominal return of 2% over the inflation rate just by holding Treasuries. 🙂

But today, CPI is 7% and the U.S. 10-year yields less than 2%. So if bond investors try to do the same thing they are losing 5% each year simply by holding Treasuries. 😬

So what is a fixed income investor or pension fund supposed to do for clients depending on these interest rates to live on in retirement? The only thing they can do: they buy stocks. Not based on individual valuations, but because they have no choice. It’s either a guaranteed loss or an unreliable and riskier source of gains. That’s part of the reason the equity prices are sky high: now bond investors are buying them out of desperation. 🤞

A classic catch-22.

Eventually stocks are expected to see a “repricing event” back down to more realistic fundamentals-based valuations, which would likely plunge us into a recession or depression… but only if the government allows it. They can always try to print, stimulate, and fake their way into more bailouts and universal basic income checks like last time.

But can they? Again?

Stranger things have happened. Or so I’ve read.

"All good books are alike in that they are truer than if they had really happened and after you are finished reading one you will feel that all that happened to you and afterwards it all belongs to you."

—Ernest Hemingway, A Letter from Cuba (1934)

Until next time 🤙,

Recommended Resources For Plan ₿

Swan. I became an official Swan partner because I love them so much. So if you're like me and just want an easy, automated way to buy bitcoin on the regular with the lowest fees in the game, head to https://swanbitcoin.com/Mulvey to get $10 in bitcoin for free ✨

Fold Card. Earn bitcoin on everything. You can win up to 100% back on every purchase, and every swipe is a chance to win a whole bitcoin. I use my own Fold card to pay for almost literally everything. If you use this referral link you get 5,000 sats free ✨

Share this post